Insight article

Is the seismic sector ready for an upturn?

8 Jun 2026

By Tanya Herwanger, SVP Multi-Client & Business Development

For much of the past decade, expectations of a marine seismic recovery have repeatedly run ahead of reality. This time, the underlying conditions look genuinely more credible. Exploration is returning to the agenda, reserve replacement is again a visible concern, as is energy security, budgets are improving, frontier basins are reopening, and acreage awards are rebounding. While investors remain focused on returns and capital discipline, there are early signs that a measured return to reinvestment is underway.

Improving demand is only part of the picture. It is equally important to ask what this upturn will actually look like. It is easy and tempting as an industry to believe that upturn equals boom, but today’s upturn is unlikely to mimic the boom cycles of the past. It is also unlikely to be a uniform operator response. The demand side like the supply side has seen significant consolidation and remaining players - supermajors, independents and NOCs - are entering this cycle with different priorities, balance sheets and portfolio pressures. That matters because the upturn will not be one size fits all, nor will demand emerge evenly across basins. Instead, the cycle is more likely to begin gradually and variably, tighten quickly as reduced capacity meets recovering demand, and then settle into a longer period of firmer pricing and steadier utilisation. This assumes that the industry does not see a newcomer with non-traditional capital access. All this is good news. In its current set up the industry does not need a boom to recover; normalisation is enough.

Is the sector ready? Not fully. A decade of weak demand, low pricing and short-cycle procurement has left structural, not temporary, constraints. Fleet capacity is finite and consolidated, equipment is ageing, specialist talent is scarce, and capital will not return on sentiment alone. If the market wants sustainable seismic capacity, it must support the conditions for reinvestment.

This is not a contractor complaint. It is a value-chain reality. Delivering on an upturn will require a more honest and nuanced dialogue about the constraints, a more modern commercial framework and a more collaborative approach to investment across the value chain. The real question isn’t is the seismic industry ready for an upturn but is the oil and gas industry ready to build the model needed for a critical part of the supply chain to deliver?

People are the bottleneck we all share

People may be the tightest constraint of all. Operator teams and contractors both cut deeply through the downturn, losing capability as well as headcount. In some areas sensible use of AI may ease the constraint, but AI is not the full answer. It cannot create physical capacity where that is required, nor can it replace the remaining expertise as it retires, and it cannot replace human ingenuity. Exploration is both art and science, even in countries where geoscience for oil and gas is still an appealing career choice, time and opportunity to develop the experience and refine the art to be successful are limited. The ceiling on the upturn will be set not just by vessels and equipment, but by the people needed to design, run and interpret complex surveys safely and well.

Acquisition capacity is capped

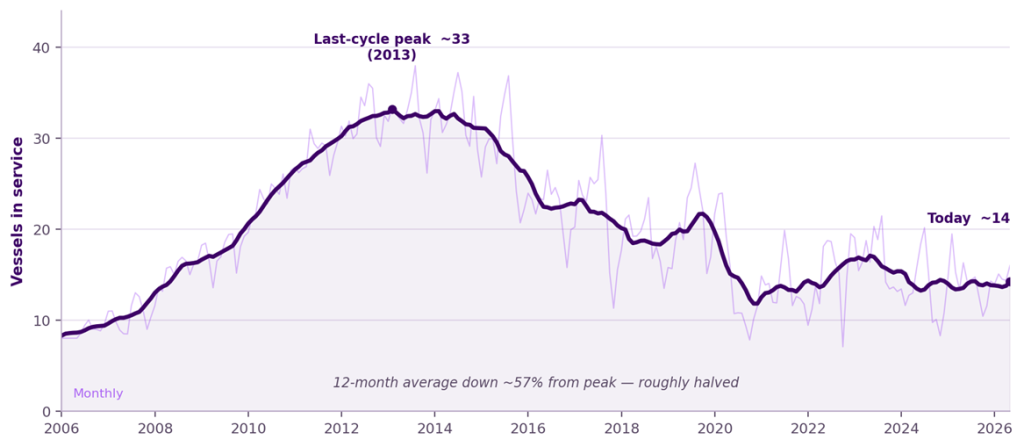

Capacity is similarly constrained. The industry has seen a massive reduction in fleet capacity since the 2013 peak. Today there are 14-16 high-end 3D vessels actively competing globally, down 50–60% from peak. Many vessels remain on the books cold stacked, but contractors are acting to rationalise their fleets. Spare capacity is leaving the industry for other markets, in many instances permanently. This is likely to continue because it makes sense given the market dynamics. For any flex capacity that remains, reactivation is neither cheap nor quick. Cold-stacked tonnage is not free capacity. Reactivation requires firm commitments and clear line of sight to returns.

Much of the available streamer equipment is mature, first spooled in the early 2010s. Across the industry the equipment base is thinner than headline vessel counts suggest. An uptick will accelerate equipment burn, and remobilised kit brings its own cost and maintenance before it is fully back in service. In practice, supply cannot simply bounce back. Large scale reinvestment in inventory will require the same commitment and certainty of returns required for reactivation.

Active high-capacity (12+ streamer) towed-streamer vessels, 2006–2026. Bold line: 12-month average. Source: S&P Global Energy CERA

In a tighter market, relative advantage will sit with companies that combine scale, proven execution and meaningful equipment depth.

The engineering has no obvious sponsor

The innovation challenge is just as real. The core architecture of modern marine acquisition - solid streamers, in-sea steering, multicomponent and broadband low-frequency sources, OBN is largely inherited from companies that no longer exist today in their original forms. The next generation of equipment has no obvious sponsor. R&D at the remaining contractors is real but deliberately modest, rightly focused on incremental gains: efficiency, reliability, environmental performance, and smaller, longer-lived OBN nodes.

On the acquisition side the industry has struggled to convert innovation into durable returns. That reality supports the incremental progress that is happening today but not large-scale reinvestment. Step change innovation, if needed or expected, will need a new framework for reliable funding.

Processing speed and imaging quality matter more than ever

Acquisition capacity is only part of the answer. Processing and imaging capabilities increasingly determine how quickly seismic data becomes decision-useful and how much value is ultimately extracted from it. Unlike acquisition, processing capacity is not capped in the same way by hardware or software; compute and workflows can scale. Unlike acquisition, processing and imaging has a different, better track record on converting innovation into returns making continued innovation likely. The tighter constraint will be people: the specialists, needed to design, run and quality-control complex workflows. There is no doubt that the next frontier to be conquered is fast access to decision-ready subsurface insight – from months to weeks. Companies with significant processing capacity, strong imaging expertise and a focus on decreasing cycle time will play an important role in this cycle.

AI is useful. It is not the answer

AI, automation and digitalisation will improve planning, processing, imaging and productivity. We invest in them and expect them to matter. But they do not create physical capacity. They cannot replace vessels, in-sea equipment or experienced crews and explorationists. The binding constraint in this cycle remains physical and human, not computational.

The OBN / towed-streamer crossover

The next five years will be shaped by the rebalancing between OBN and towed streamer. OBN is now central to development, monitoring, and increasingly exploration, while towed streamer remains the most efficient tool for wide-area work. Both matter. Both are constrained. And both draw on the same limited pool of people, vessels, equipment and capital.

The risk is that, as demand returns, the OBN market repeats the behaviours that weakened the streamer market in the past: price-led competition, poor risk allocation and too little room for reinvestment. That pressure is already visible. The strategic question is no longer whether work will shift between the two, but where, when and to what extent. Those decisions will not be uniform, but they will be critical. The industry cannot sustain both fleets at full scale under legacy commercial models, so future capacity choices will need to be made more deliberately - and more collaboratively.

What does it take to deliver on an upturn

None of this is cause for pessimism. It is a call for realism. If the sector is to deliver the next phase of demand well, three things need to change together.

First, treat capacity as strategic infrastructure, not spot supply

Short-cycle tenders and price-led procurement have reached their limit. The issue is not vessel access for its own sake. It is access to seismic that improves and accelerates decisions in a more disciplined exploration environment. That matters even more as permitting, environmental opposition and access restrictions make activity less predictable. If operators want dependable access to seismic, they need to move from transactional access to planned capacity that optimises utilisation and supports reinvestment in both equipment and people. This logic is not new. Operators know very well how to create value from strategic infrastructure, pipelines, FPSOs and export routes are planned, shared and optimised over time. Seismic capacity should be viewed in the same way.

Second, evolve the business models

The industry has not innovated commercially for decades. The multi-client model was transformative in its time, but today’s market is different, explorers are few, exploration is more concentrated and targeted, access routes have changed, and the classic speculative, multiple-sales model no longer fits. This sits alongside short cycle tenders and price led procurement which also no longer fits. The replacement will not be a single model. Different operator groups will require different models depending on strategic priorities, basin maturity, subsurface risk, time horizon and their own constraints. In some settings, shared access to data may still work; in others, shared access to assets may provide a more appropriate option; for others longer term capacity reservation may be best. What matters is that the commercial structure reflects the strategic value of the seismic work being undertaken, rather than treating all demand as interchangeable spot procurement.

Third, mature the technology conversation

AI, automation, digitalisation, lower-emission operations, smaller nodes, longer battery life, and better algorithms all matter. None substitutes for crew, steel, optimised utilisation and a financially robust supply chain. The useful discipline is to be clear about which problems technology can solve and which still require capital, assets and long-term commitment.

So, are we ready?

The sector is leaner, more disciplined and as technically capable as ever. As exploration activity recovers and offshore demand strengthens across both streamer and OBN, the supply side will tighten quickly. This tightening is needed to stabilise returns in the industry after a prolonged period of weak demand and structural contraction, but it needs to be managed to ensure continued access to high-quality seismic data.

An upturn looks real. Delivering it will require a more honest dialogue about the existing constraints, a more modern commercial framework and a more collaborative approach to investment across the value chain. There is no one-size-fits-all answer. Supermajors, independents and NOCs have different drivers and different considerations, but all have the shared goal of continued access to high quality seismic data which remains the primary tool for subsurface understanding and derisking.

Companies like Shearwater with real fleet scale, operational depth, significant processing capacity, strong imaging expertise and carefully curated library positions are well placed to help meet the upturn.

We are ready to invest, execute and grow with the market. But to deliver, Contractors and operators alike must stop expecting legacy models to solve a fundamentally new problem.

Related articles

Science and seismic innovation for smarter and faster energy exploration

Shining a light on energy poverty: the journey to Gopeng